A Budget for all as Singapore tackles immediate cost-of-living challenges, invests in longer-term goals

By Goh Yan Han, Political Correspondent, The Straits Times, 17 Feb 2024

Everyone will have a slice of the Budget 2024 pie, which aims to address immediate challenges like cost-of-living pressures while investing in longer-term goals of strong economic growth, better jobs and a culture of lifelong learning.

Key policy moves include enhancements to the Assurance Package like giving out more Community Development Council (CDC) vouchers.

A significant top-up of SkillsFuture credits will benefit mid-career workers, while a corporate income tax rebate aims to help companies manage rising costs.

The Government will also be rolling out strategies to improve retirement adequacy, lower healthcare costs and provide more for lower-wage workers.

Many of these moves were signposted earlier in the Forward Singapore report released in October 2023.

Budget 2024 rolls out the first instalment of the Forward Singapore programmes, Deputy Prime Minister Lawrence Wong said in Parliament on Feb 16 as he delivered his third annual Budget speech.

He laid out a $131.4 billion proposal – about 18.3 per cent of Singapore’s gross domestic product.

These moves are part of an “ambitious agenda” to achieve the shared goals of building a nation that is vibrant and inclusive, fair and thriving, as well as resilient and united, he said.

They come amid a mixed outlook for 2024, he said. Growth in major economies is expected to be resilient, but geopolitical risks continue to loom large.

At the same time, global inflationary pressures are tipped to further recede, said DPM Wong, who is also Finance Minister.

He was “cautiously optimistic” that 2024 will be better than 2023, as he projected a $0.8 billion surplus for the upcoming financial year – “essentially a balanced fiscal position”.

Tackling cost-of-living pressures

DPM Wong acknowledged the pressure of higher living costs faced by many households.

While the economic situation is expected to improve in 2024, there are still uncertainties, which is why he has further enhanced the Assurance Package, said DPM Wong.

The package, meant to offset the impact of the goods and services tax hike, will be boosted by another $1.9 billion.

This includes an additional $600 in CDC vouchers for all Singaporean households, with the first tranche of $300 to be disbursed in end-June, and the remainder in January 2025.

All adult Singaporeans with an assessable income of up to $100,000 and who do not own more than one property will also receive a Cost-of-Living Special Payment of between $200 and $400 in cash.

Other measures to help individuals with costs include a MediSave top-up of up to $300 for about 1.4 million adult Singaporeans aged 21 to 50.

Those aged 51 and above will receive up to $1,500 in their Medisave Accounts under the earlier announced Majulah Package.

To help parents, fee caps – the maximum amount that school operators can charge – will be reduced for government-supported pre-schools. There will also be fee reductions for special education schools.

In addition, there will be a personal income tax rebate of 50 per cent, capped at $200, for the 2024 year of assessment.

Businesses will also receive help to manage rising costs, such as a 50 per cent corporate income tax rebate, capped at $40,000.

Supporting workers and businesses

A key component of the Budget is a suite of measures targeted at mid-career workers.

All Singaporeans aged 40 and above will receive a $4,000 top-up in SkillsFuture Credit as part of a new SkillsFuture Level-Up programme.

This will benefit about 1.95 million Singaporeans currently, though those younger will receive the top-up as well when they turn 40.

While the existing basic tier of $500 SkillsFuture Credit covers a wide range of courses, the new credit will only be allowed for use for selected training programmes with better employability outcomes. More details will be announced later.

Under the new programme, there will be subsidies for all Singaporeans aged 40 and above to pursue another full-time diploma at polytechnics, institutes of technical education and arts institutions from the 2025 academic year onwards. Currently, only those studying for their first diploma benefit from government subsidy.

DPM Wong also unveiled a monthly training allowance for Singaporeans aged 40 and above who enrol in selected full-time courses.

These moves are meant to help Singaporeans develop to their fullest potential, and to have productive and meaningful careers, he said.

A key priority of the Government is to ensure a strong, innovative and vibrant economy – and it will do so by focusing on productivity and innovation, he added.

DPM Wong announced a new Refundable Investment Credit, a tax credit meant to help Singapore stay competitive and attract investments from global companies.

There will also be investments to upgrade the Nationwide Broadband Network to enable mass market access to broadband speeds of up to 10 gigabits per second in the second half of this decade. This would be 10 times faster than the broadband speed in most homes today.

DPM Wong also brought up the temporary financial support scheme for the involuntarily employed, which had been mentioned in the Forward SG report.

He said that the Government is working out the parameters for the scheme, and will provide more details later in the year.

“Ours must always be an economy that provides opportunities for all; an economy that benefits the many rather than the few,” he said.

In this vein, DPM Wong announced enhancements to schemes that uplift lower-wage workers, such as the Workfare Income Supplement scheme and Workfare payouts.

The Government will also provide more support for employers who raise the wages of lower-wage workers by increasing its co-funding levels of the Progressive Wage Credit Scheme – from a maximum of 30 per cent to 50 per cent.

To encourage and support more young ITE graduates in upskilling efforts, a new ITE Progression Award will be rolled out for those aged 30 and below.

This will include a $5,000 top-up to their Post-Secondary Education Accounts when they enrol in a diploma programme, as well as a further $10,000 top-up to their Central Provident Fund (CPF) Ordinary Account when they attain their diplomas.

Help for seniors

Another area that the Budget provides for is support for the retirement needs of senior citizens.

DPM Wong said there will be adjustments to the CPF system, such as an increase in CPF contribution rates for those aged 55 to 65 by 1.5 percentage points in 2025.

Employers will be able to benefit from the CPF Transit Offset for another year, to cover half of the increase in their contributions for 2025. This will help cushion the impact on business costs.

The Enhanced Retirement Sum – the maximum amount one can put in the CPF retirement account to receive CPF payouts – will also be raised from 2025, to become four times the Basic Retirement Sum (BRS). It is currently three times the BRS.

The CPF system will also be tweaked, as the Special Account will be closed for those aged 55 and above, starting in 2025. The savings in the Special Account will be transferred to the Retirement Account, up to the Full Retirement Sum. The rest will be transferred to the Ordinary Account.

In addition, there will be enhancements to retirement support schemes for seniors who need more help. These include the Silver Support Scheme and Matched Retirement Savings Scheme.

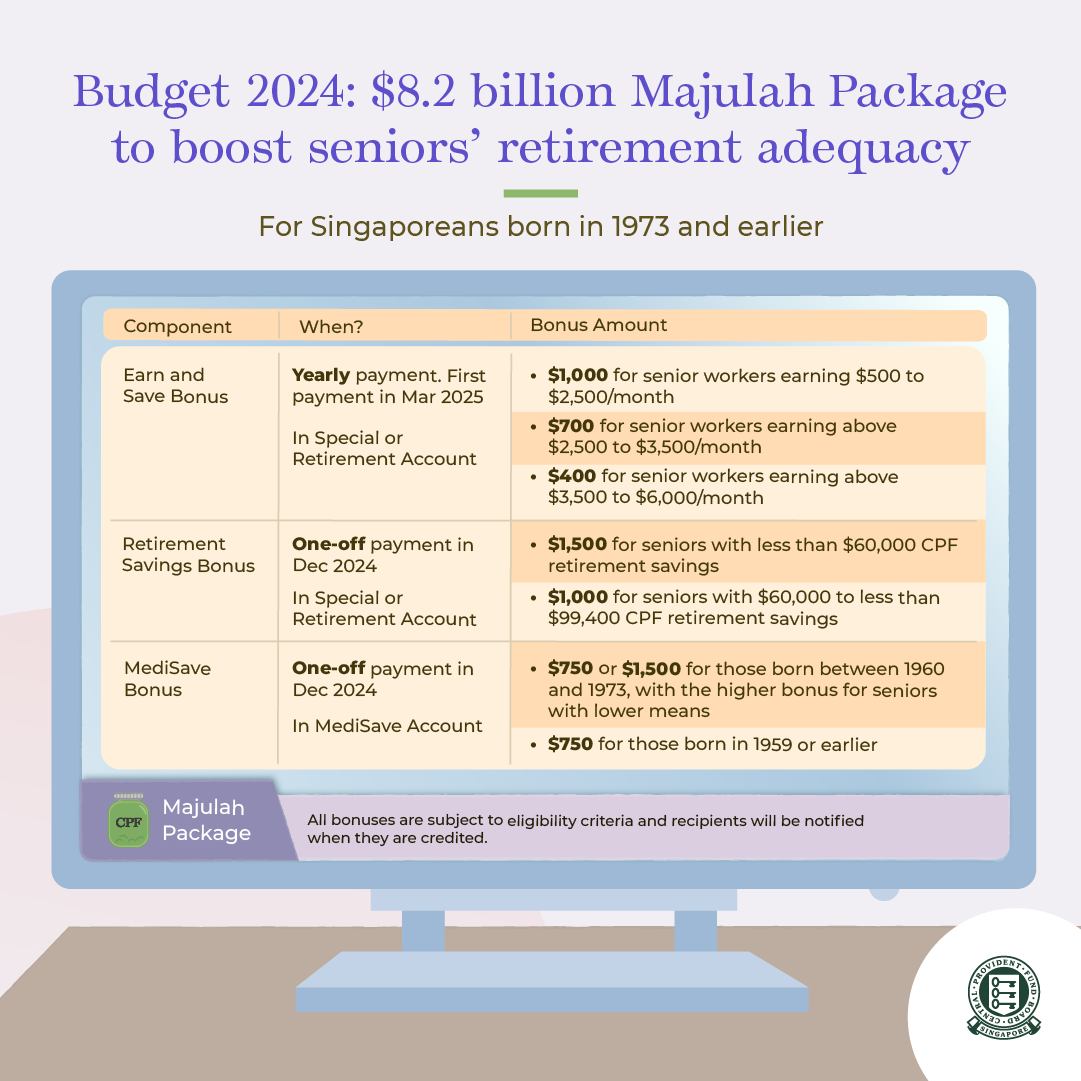

DPM Wong also provided more details on the Majulah Package, announced by Prime Minister Lee Hsien Loong at the National Day Rally in 2023. The scheme will benefit about 1.6 million Singaporeans.

The package includes an Earn and Save Bonus for seniors earning up to $6,000 a month to accumulate more retirement savings and a one-time Retirement Savings Bonus of between $1,000 and $1,500 for seniors with retirement savings below the BRS.

Rounding up his speech, DPM Wong said the Forward Singapore policy moves will cost around $5 billion in the 2024 financial year, and will in total reach close to $40 billion by the end of the decade.

Projections by the Finance Ministry in 2023 assessed that government spending would increase to around 20 per cent of GDP by 2030.

DPM Wong said that for now, that remains the Government’s assessment.

Assuming the Government stays within this range of spending increase, it should have sufficient revenues to maintain a balanced budget over the coming years, he added.

But the medium-term fiscal position is tight, as there are many pressures to spend more.

“We will have to manage these expenditures carefully, or we will end up with a significant funding gap,” he said.

This is already happening in many other advanced economies, where public finances are on an unsustainable path and fiscal systems are at risk of breaking, he added.

“We must never allow this to happen in Singapore. Instead, let us uphold the ethos of fiscal discipline and responsibility that has served us well, and ensure that our fiscal position always remains balanced, sound and sustainable.”

He reiterated that Singapore has been able to weather past storms and emerge stronger.

“I believe we can do so again in our road ahead, so long as we stay united, work together and continue to keep faith in each other.”

Parliament will debate the Budget and the spending plans of various ministries from Feb 26 to March 7.